Global equity markets decline in August but the trend for the Dollar remains intact – Month in Review: August 2023

Macroeconomic Environment Review

Global equity markets declined in August, as investors grappled with a combination of factors, including concerns about rising interest rates, the ongoing war in Ukraine, and the potential for a global recession. Conversely, the US dollar continued to rally as investors bet on the relative strength of the US economy and the Federal Reserve’s commitment to fighting inflation. The US dollar index rose more than 5% in August. The dollar also strengthened against most emerging market currencies. There are several factors driving the dollar’s strength. First, the US economy is outperforming other major economies. The US unemployment rate is at a 50-year low, and economic growth is expected to remain strong in the coming quarters. Second, the Federal Reserve is raising interest rates more aggressively than other central banks. This makes US assets more attractive to investors, who are seeking higher yields. Third, the US government is running a large budget deficit. This is putting upward pressure on long-term interest rates, which also makes the dollar more attractive to investors. Finally, the dollar’s strength is also being supported by the war in Ukraine, which has created uncertainty in global markets and led investors to seek the safety of the dollar. Elsewhere, the euro fell to its lowest level against the dollar in 20 years, while the Japanese yen also weakened significantly.

Looking ahead, we expect the dollar to remain strong in the near term. However, there are some risks to the dollar’s outlook. If the US economy were to slow down significantly, or if the Federal Reserve were to pause its interest rate hikes, the dollar could weaken. Furthermore, the dollar’s strength is a mixed blessing for the US economy: on one hand, it makes US exports more expensive and could lead to slower economic growth; on the other hand, though, it makes US imports cheaper and could help to keep inflation under control. On balance, however, we believe that the dollar’s strength is likely to continue in the coming months, but the pace of the rally is likely to moderate while markets are likely to remain volatile as investors grapple with the uncertainty surrounding the global economy.

Monthly Performance Review

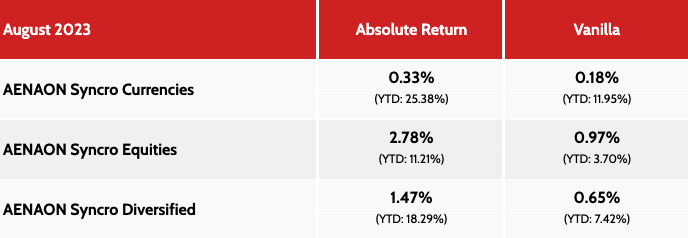

During the month of August 2023, AENAON Syncro Strategies generated the following total returns net of fees:

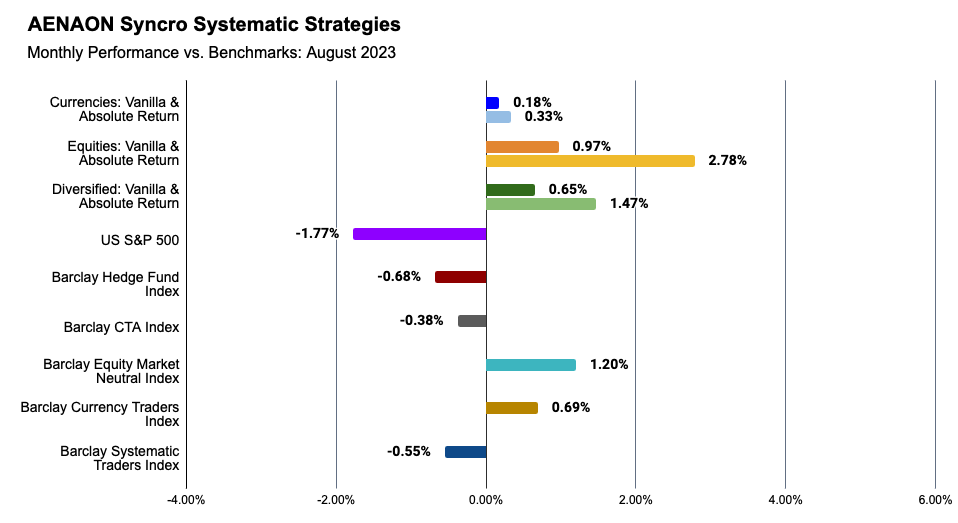

Across the spectrum of our benchmark indices, our strategies’ performance during August was positive. As a comparison, the US S&P 500 equities index dropped by 1.77%, the Barclay Hedge Fund Index posted a 0.68% decline, the Barclay CTA Index lost 0.38% while the other benchmark indices can be seen on the chart below.

Further to the above, and as we were notified during the past month, AENAON’s strategies received yet another 2 awards from the prestigious BarclayHedge community: AENAON Syncro Equities, our quantitative US Equities model, has ranked number 2 in the Equity Market Neutral category, and AENAON Syncro Diversified, our quantitative FX and Equities Model has ranked number 5 in the Multi-Strategy category for July 2023 among hundreds of our peers, underlining our robust performance over the past years that continues strong.

Chart 1: Monthly Performance vs. Benchmark Indices – August 2023

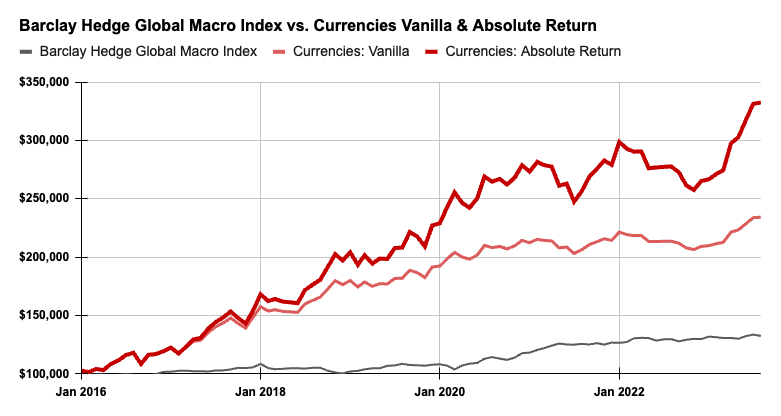

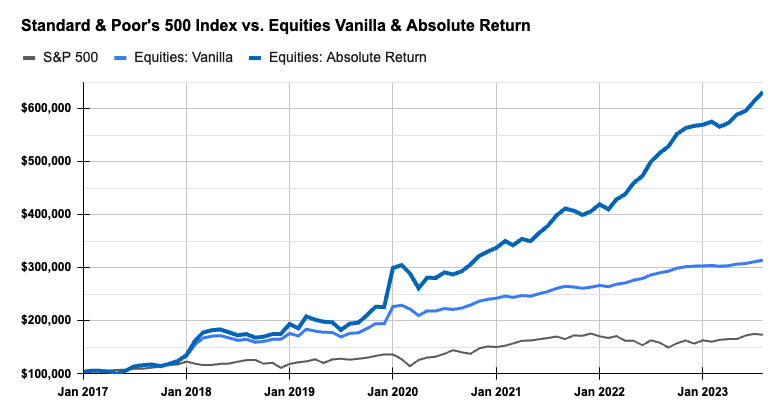

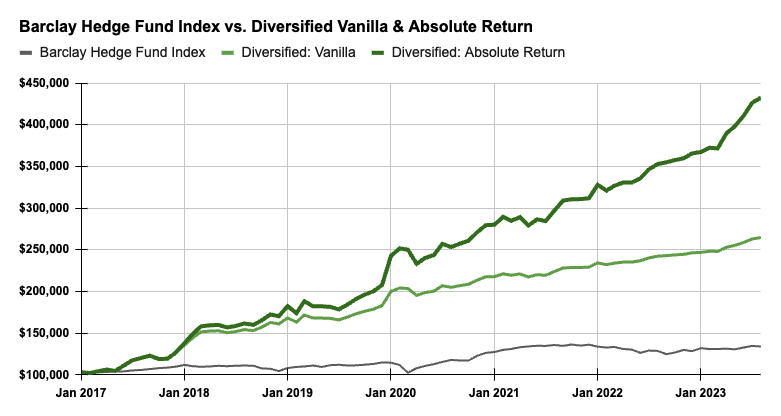

Charts 2, 3 and 4: Inception-to-Date Performance vs. Benchmark Indices

You can always review our updated factsheets at the following Fundpeak links, with monthly performance updates and statistics since inception: