Inflation expectations at the forefront – Month in Review: February 2021

Macroeconomic Environment Review

Over the past month, news headlines revolved around the upbeat global growth prospects in tandem with the improved geopolitical and macro sentiment. Investors grew optimistic as there’s progress, albeit slow, in the number of Covid-19 vaccinations while fresh economic data and recent surveys also pointed towards a global recovery. Of course, elevated inflation concerns have somewhat tempered optimism but it seems that the major central banks will take their time before tightening policy, allowing for their respective economies to “run hot” in the interim.

With the economic backdrop looking more favorable for some countries, while others still lack momentum, the US Dollar traded mostly unchanged on average against its peers. The Euro trod water on either side of the 1.20 mark, the Pound and the Australian dollar did capture some gains while the Yen saw extended weakness. However, with speculative positioning still heavily short on the greenback, the question is whether there’s more risk to the upside or the downside for the US currency going forward. And to be able to answer that, we need to take a look at some of its major counterparts.

From a macroeconomic perspective, there are a few notes I’d like to make here: despite the delay in the Covid-19 response from the European policymakers, the outlook still remains bullish for the Euro. The twin US deficit is a major drag for the Dollar and with money markets now focusing on the post-Coronavirus era, a move higher looks more likely in the medium term, so the Dollar might take a hit here.

At the same time though, Sterling appears better positioned to benefit from the US’ macro burdens and Euro’s transient lag in momentum. With vaccinations progressing rapidly in the UK and global risk appetite improving, I reckon that Sterling/Dollar and Euro/Sterling may present interesting opportunities in the short term.

Finally, I think it’d be good to keep an eye on the Yen, which despite a positive macro outlook looks vulnerable at the moment; having said that though, a timely reversal in the Dollar’s momentum could allow for a correction in favor of the Japanese currency so opportunities may be around the corner here.

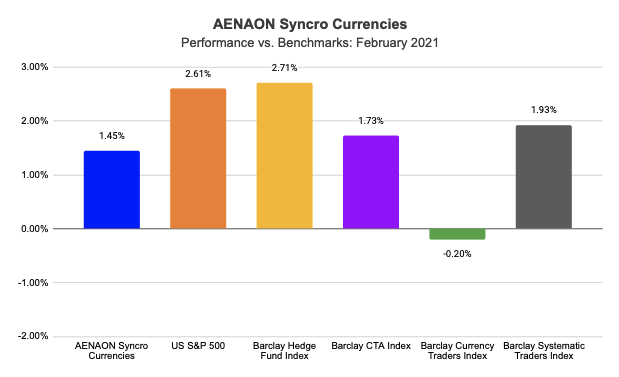

Performance Review February 2021

Across the spectrum of our benchmark indices, our performance during January was positive. As a comparison, AENAON Syncro Currencies returned 1.45% last month, versus a 2.61% return for the US S&P 500 equities index, a 2.71% gain for the Barclay Hedge Fund Index, a 1.73% advance for the Barclay CTA Index, a -0.20% loss for the Currency Traders Index and a 1.93% gain for the Systematic Traders Index.

Chart 1: Performance vs. Benchmark Indices – February 2021

You can always review AENAON Syncro Currencies’ updated factsheet at our Fundpeak link, with monthly performance updates and statistics since inception.