The dollar looks towards further strength going into this year’s final quarter – Month in Review: September 2022

Macroeconomic Environment Review

Financial and currency markets are on a roller coaster driven by the fear of recession and hopes that central banks will have to slow the pace of tightening soon. Policy actions have compounded the volatility and forced central banks to intervene. The pillars of USD support are still in place, but we fear that central banks underestimate the collective impact of their tightening. The result could be a worse-than-expected recession. This would be USD bullish if the US is still seen outperforming or USD bearish if the Fed is forced to make a radical U-turn.

Looking through the volatility of the last few weeks we believe that the two main pillars of USD support remain in place. First, the global economy is in a downturn possibly heading for recession and the US economy continues to outperform. Indeed, while Europe is preparing for a chilly winter recession, the US economy remains surprisingly resilient. This is most evident in the labor market with first-time jobless claims dropping from more than 250.000 to less than 200.000 over the last three months.

Second, while the Fed may not guide markets to expect even more rate hikes, its policy stance remains clearly hawkish and interest rates in the US are likely to stay ahead of interest rates in most other places. In addition to these two pillars, recent relative improvements on the external side have supported the USD as well. While soaring energy costs have squashed the current account surpluses of the Euro area and Japan, rising net export revenues from oil and gas have reduced the US current account deficit.

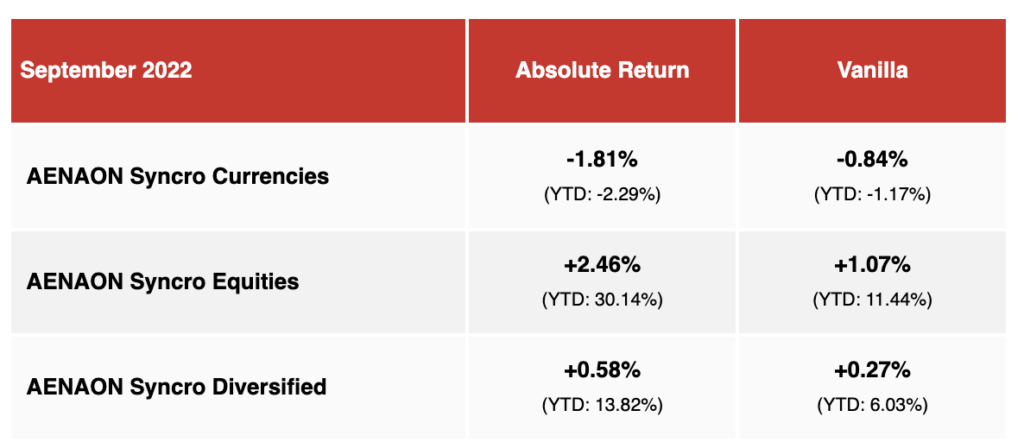

Monthly Performance Review

During the month of September 2022, AENAON Syncro Strategies generated the following total returns net of fees:

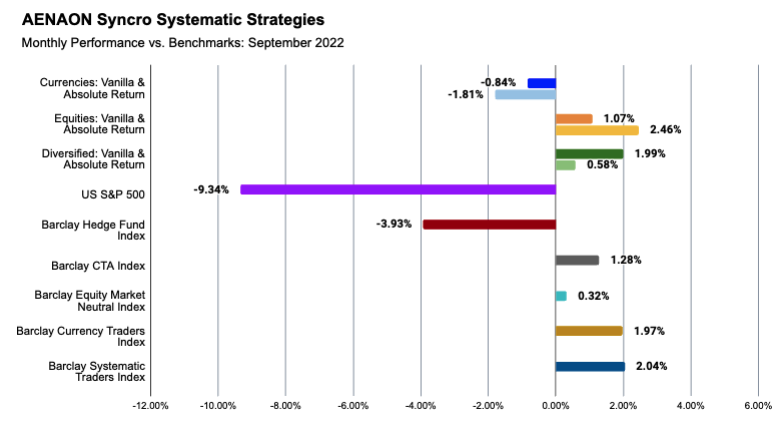

Across the spectrum of our benchmark indices, our strategies’ performance during September was mildly positive. As a comparison, the US S&P 500 equities index lost -9.34%, the Barclay Hedge Fund Index posted a -3.93% decline, the Barclay CTA Index added 1.28% while the other benchmark indices can be seen on the chart below.

Chart 1: Monthly Performance vs. Benchmark Indices – September 2022

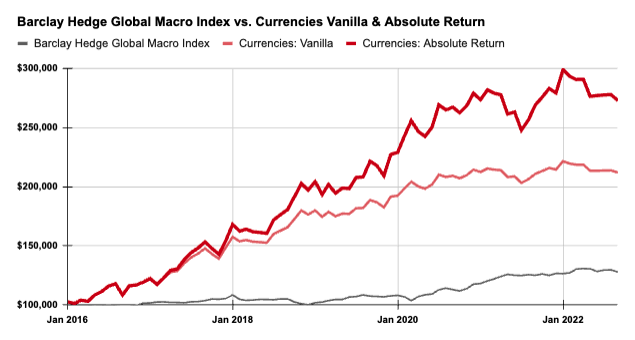

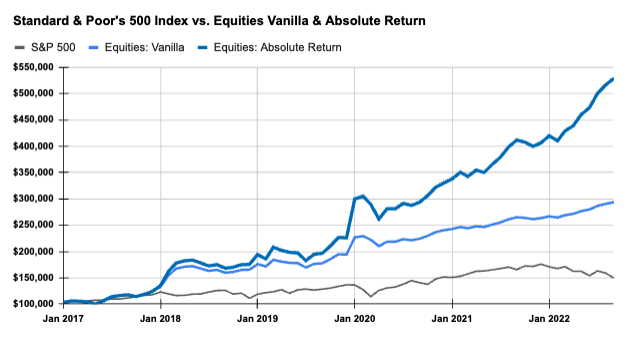

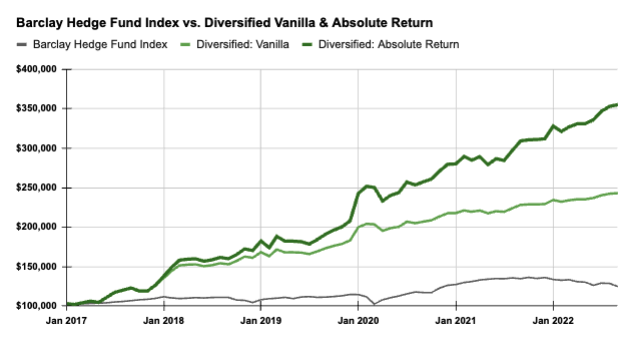

Charts 2, 3 and 4: Inception to Date Performance vs. Benchmark Indices

You can always review our updated factsheets at the following Fundpeak links, with monthly performance updates and statistics since inception: