US economy picks up pace, Europe lags behind – Month in Review: March 2021

Macroeconomic Environment Review

Last month was a strong one for the traditional asset classes on the back of the positive bias we discussed in our previous monthly communication. Led by the massive stimulus package, the US economy seems to be building momentum with retail sales picking up substantially: Bloomberg reported that credit and debit card data from Bank of America for the week ending 20 March showed total spending rose not only 45% from the COVID shutdown period a year ago, but also climbed 23% from two years ago, driven by government stimulus payments. This has translated into strong gains for US equities in March and it falls in line with the broader uptick in demand as economies are attempting to reopen after Covid-19.

Having said that, the situation in Europe remains complicated and potential recovery to pre-Covid conditions appears months away. This has led the Dollar to gain further against the Euro, with prices dropping as low as 1.17. Granted, the first few sessions of the current month have allowed for a covering rally in the Euro but unless things change dramatically in the coming weeks, the Single currency will remain under pressure.

It is also imperative to keep in mind here that with the massive US stimulus package being deployed and the economy picking up pace again, a higher than anticipated inflation rate might force the Fed to act sooner rather than later. And an increase in US rates could further prop the Dollar higher, which would result in further pressure on the other currencies lagging behind in momentum. So, we should remain on the lookout for further opportunities on that side of the trade but not get carried away: the longer-term outlook for the US currency looks bleak as the huge current account deficit and the – eventual – improvement in risk conditions on a global scale will, at some point, force it to give up any recent gains.

Performance Review March 2021

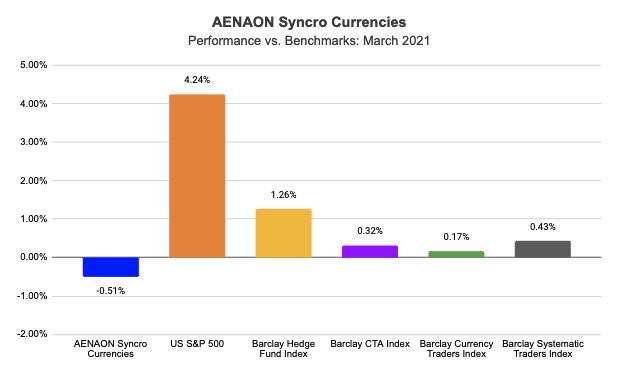

Across the spectrum of our benchmark indices, our performance during March was a bit lackluster. As a comparison, AENAON Syncro Currencies returned -0.51% last month, versus a 4.24% return for the US S&P 500 equities index, a 1.26% gain for the Barclay Hedge Fund Index, a 0.32% advance for the Barclay CTA Index, a 0.17% gain for the Currency Traders Index and a 0.43% uptick for the Systematic Traders Index.

Chart 1: Performance vs. Benchmark Indices – March 2021

You can always review AENAON Syncro Currencies’ updated factsheet at our Fundpeak link, with monthly performance updates and statistics since inception.