A mixed bag for FX and US equities markets – Month in Review: April 2024

Macroeconomic Environment Review

April 2024 proved to be a month of mixed signals and cautious optimism in financial markets. While the Federal Reserve’s hawkish stance on inflation was anticipated, the lack of clarity on the timing of future rate cuts sent shockwaves through various asset classes.

In the foreign exchange market, the story wasn’t a simple dollar dominance. The Euro and Japanese Yen experienced some appreciation against the US Dollar. This can be attributed to several factors. Firstly, the delayed rate cuts in the US lowered the attractiveness of the Dollar as a haven currency. Secondly, concerns about slowing global growth due to the ongoing war in Ukraine and broader geopolitical uncertainties may have pushed investors toward traditional safe havens like the Yen. Additionally, rising commodity prices, particularly oil, may have put upward pressure on currencies pegged to resource exports, such as the Canadian Dollar and the Norwegian Krone. However, it’s important to note that the overall appreciation for these currencies against the USD was relatively modest.

The US equity market, on the other hand, faced a significant correction throughout April. The S&P 500 ended the month over 4% lower, wiping out much of its year-to-date gains. This decline can be primarily attributed to the revised outlook on interest rates. Sectors sensitive to rate changes, like technology and real estate, were hit the hardest. Growth stocks, previously valued based on future earnings potential, saw their valuations decline as investors priced in the possibility of higher borrowing costs. While inflation remained a concern, it wasn’t enough to outweigh the negative impact of the Fed’s policy shift on investor confidence.

The coming months will be crucial in determining the direction of both the FX and US equity markets. The Fed’s next policy meeting and any updates on the ongoing geopolitical situation will be closely watched by investors. If the Fed maintains its hawkish stance, further volatility can be expected, particularly in interest rate-sensitive sectors of the US equity market. However, if the Fed signals a more balanced approach or if progress is made on the geopolitical front, a potential rebound could be in the cards for both markets.

Monthly Performance Review

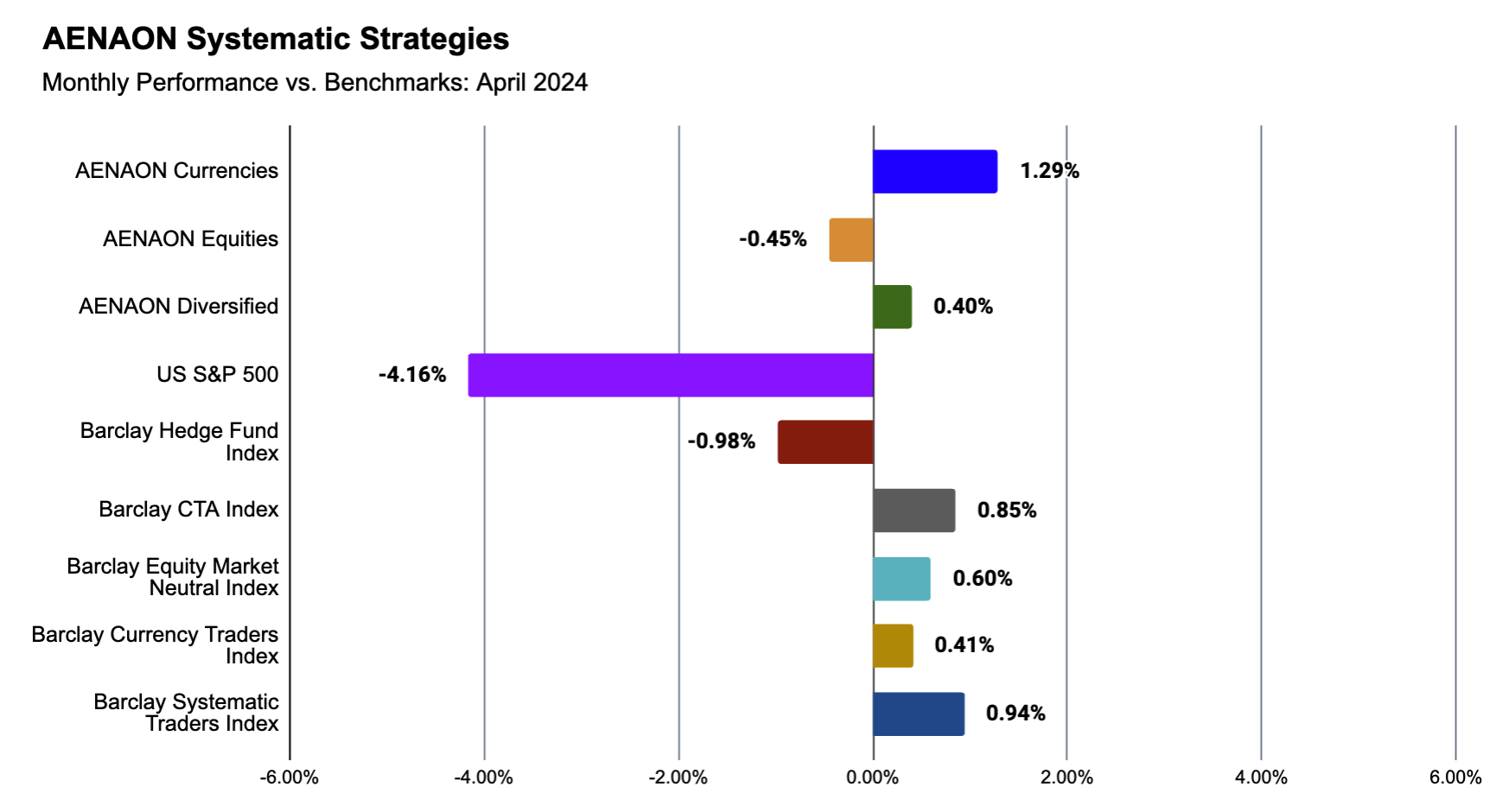

During April 2024, AENAON Systematic Strategies generated the following total returns:

Across the spectrum of our benchmark indices, our strategies’ performance during March was strongly positive. As a comparison, the US S&P 500 equities index lost -4.16%, the Barclay Hedge Fund Index posted a -0.98% decline, the Barclay CTA Index added 0.85% while the other benchmark indices can be seen on the chart below.

Chart 1: Monthly Performance vs. Benchmark Indices – April 2024

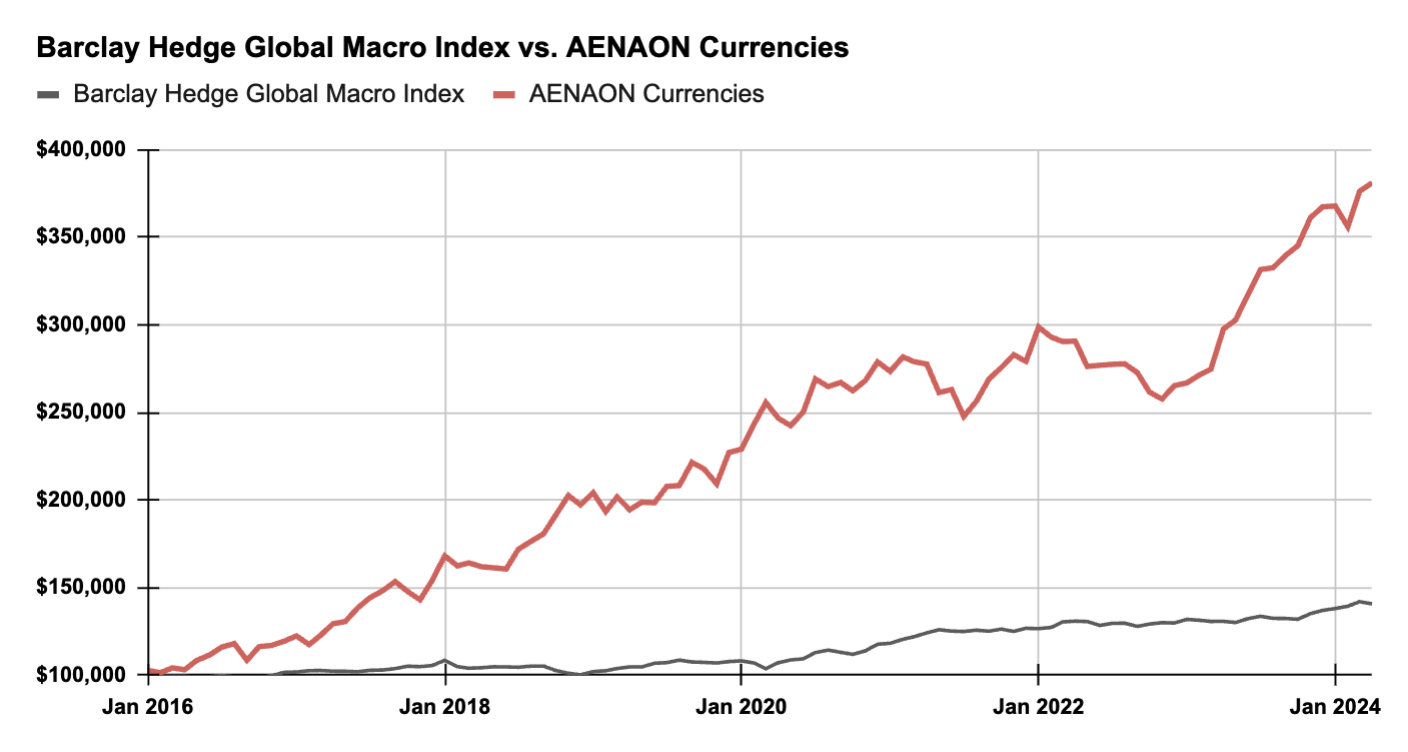

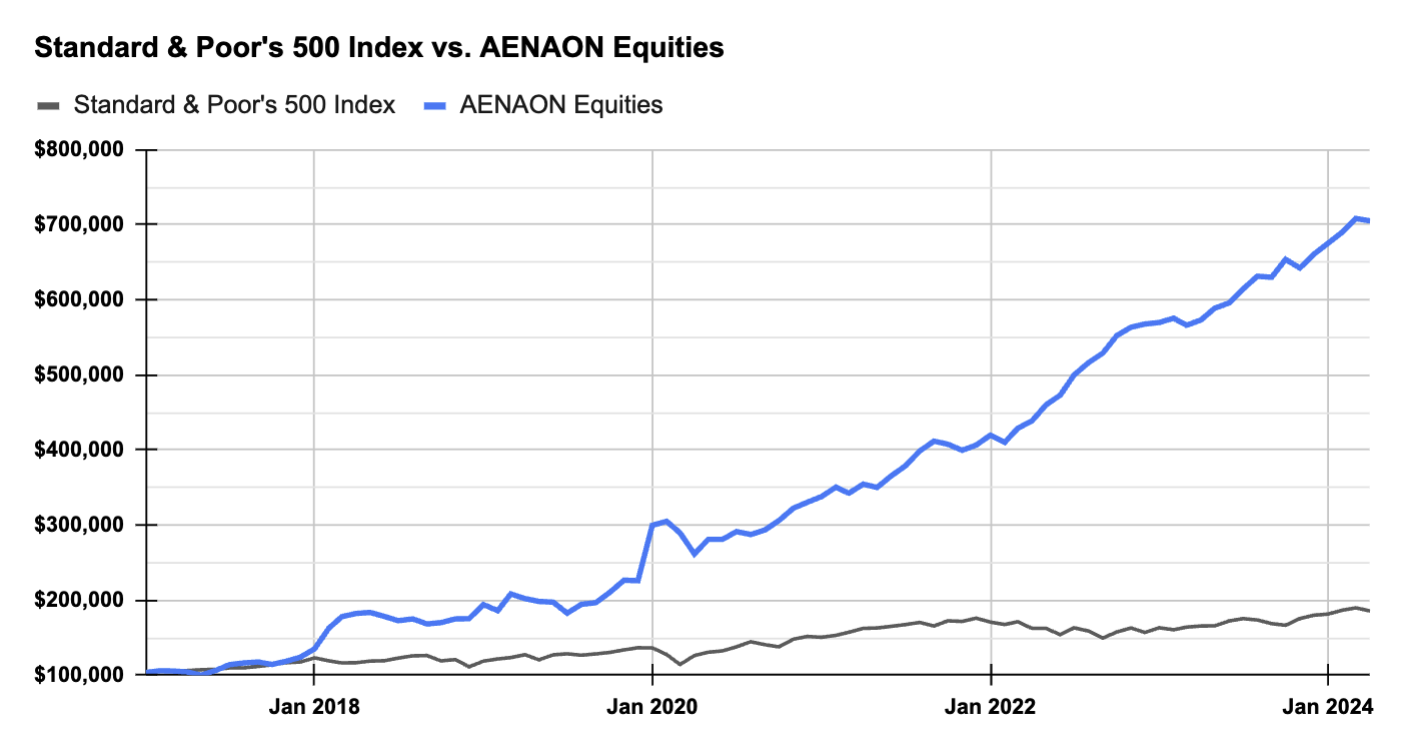

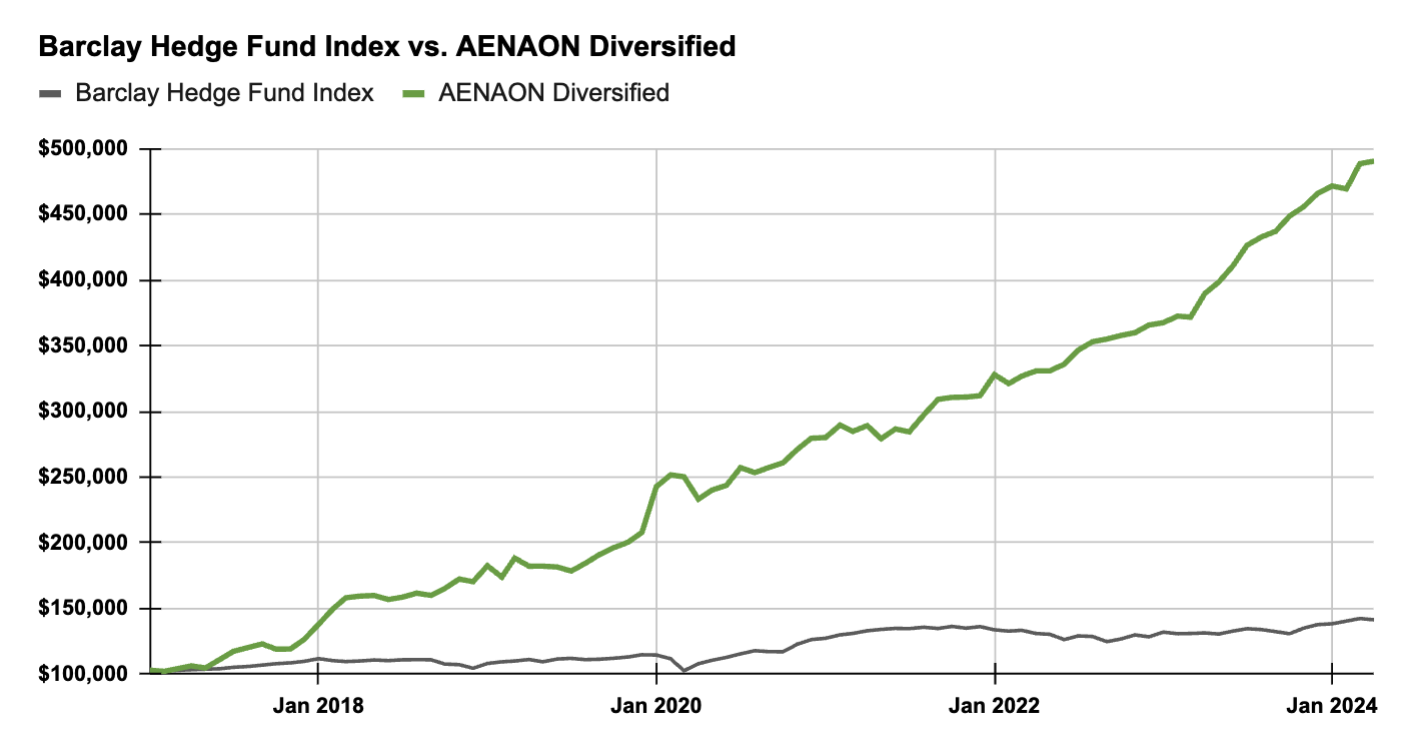

Charts 2, 3 and 4: Inception-to-Date Performance vs. Benchmark Indices

You can always review our updated factsheets at the following Fundpeak links, with monthly performance updates and statistics since inception: